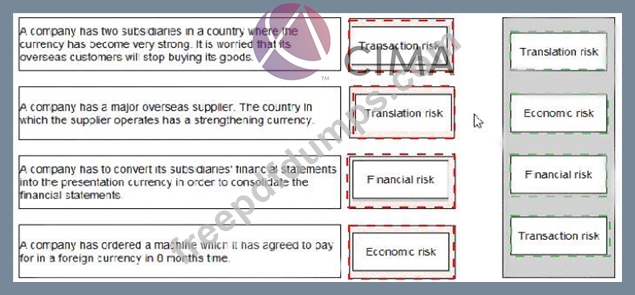

F3 Exam Question 101

Select the category of risk for each of the descriptions below:

F3 Exam Question 102

A company's Board of Directors wishes to determine a range of values for its equity.

The following information is available:

Estimated net asset values (total asset less total liabilities including borrowings):

* Net book value = $20 million

* Net realisable value = $25 million

* Free cash flows to equity = $3.5 million each year indefinitely, post-tax.

* Cost of equity = 10%

* Weighted Average Cost of Capital = 7%

Advise the Board on reasonable minimum and maximum values for the equity.

The following information is available:

Estimated net asset values (total asset less total liabilities including borrowings):

* Net book value = $20 million

* Net realisable value = $25 million

* Free cash flows to equity = $3.5 million each year indefinitely, post-tax.

* Cost of equity = 10%

* Weighted Average Cost of Capital = 7%

Advise the Board on reasonable minimum and maximum values for the equity.

F3 Exam Question 103

It is now 1 January 20X0.

Company V, a private equity company, is considering the acquisition of 40% of the equity of Company A for a total amount of $15 million.

Company A has been established to develop a new type of engine which will be launched at the end of 20X1.

Company A is forecasting that the new engine will result in free cash flows to equity of $2m in its first year of operation and that this will rise by 8% per year for the foreseeable future.

The new engine is the only commercial activity that Company A is involved in.

Company V intends to sell its stake in Company A when the new engine is launched.

Company A has a cost of equity of 12%.

Assuming that Company V receives an amount that reflects the present value of their shares in company A.

what is the estimated annual rate of return to Company V from this investment? (To the nearest %)

Company V, a private equity company, is considering the acquisition of 40% of the equity of Company A for a total amount of $15 million.

Company A has been established to develop a new type of engine which will be launched at the end of 20X1.

Company A is forecasting that the new engine will result in free cash flows to equity of $2m in its first year of operation and that this will rise by 8% per year for the foreseeable future.

The new engine is the only commercial activity that Company A is involved in.

Company V intends to sell its stake in Company A when the new engine is launched.

Company A has a cost of equity of 12%.

Assuming that Company V receives an amount that reflects the present value of their shares in company A.

what is the estimated annual rate of return to Company V from this investment? (To the nearest %)

F3 Exam Question 104

A listed company follows a policy of paying a constant dividend. The following information is available:

* Issued share capital (nominal value $0.50) $60 million

* Current market capitalisation $480 million

The shareholders are requesting an increased dividend this year as earnings have been growing. However, the directors wish to retain as much cash as possible to fund new investments. They therefore plan to announce a

1-for-10 scrip dividend to replace the usual cash dividend.

Assuming no other influence on share price, what is the expected share price following the scrip dividend?

Give your answer to 2 decimal places.

* Issued share capital (nominal value $0.50) $60 million

* Current market capitalisation $480 million

The shareholders are requesting an increased dividend this year as earnings have been growing. However, the directors wish to retain as much cash as possible to fund new investments. They therefore plan to announce a

1-for-10 scrip dividend to replace the usual cash dividend.

Assuming no other influence on share price, what is the expected share price following the scrip dividend?

Give your answer to 2 decimal places.

F3 Exam Question 105

An entity prepares financial statements to 31 December each year. The following data applies:

1 December 20X0

* The entity purchased some inventory for $400,000.

* In order to protect the inventory against adverse changes in fair value the entity entered into a futures contract to sell the inventory for a fixed price on 31 January 20X1.

* The entity designated this contract as a fair value hedge of the value of the inventory.

31 December 20X0

* The inventory had a fair value of $480,000 and the futures contract had a fair value of $75,000 (a financial liability).

What will be the impact on the statement of profit or loss and other comprehensive income for the year ended

31 December 20X0 in respect of the change in the value of the inventory and the futures contract?

1 December 20X0

* The entity purchased some inventory for $400,000.

* In order to protect the inventory against adverse changes in fair value the entity entered into a futures contract to sell the inventory for a fixed price on 31 January 20X1.

* The entity designated this contract as a fair value hedge of the value of the inventory.

31 December 20X0

* The inventory had a fair value of $480,000 and the futures contract had a fair value of $75,000 (a financial liability).

What will be the impact on the statement of profit or loss and other comprehensive income for the year ended

31 December 20X0 in respect of the change in the value of the inventory and the futures contract?